Life Insurance Should Not Be Harder Than An Instrument Rating.

From student pilots building toward certificates to CFIs building flight time to career aviators planning long-term, you face financial risks most insurance agents don't understand. As a pilot and AGI, I provide the insurance and risk management guidance you need, from someone who speaks your language and understands your journey.

The problem

You've spent months mastering unusual attitudes, emergency procedures, and complex systems to earn your ratings. But when you apply for life insurance, agents who've never sat in a cockpit treat your aviation activity like a risk assessment checkbox...

Pilot First. Advisor Second. Fiduciary Always.

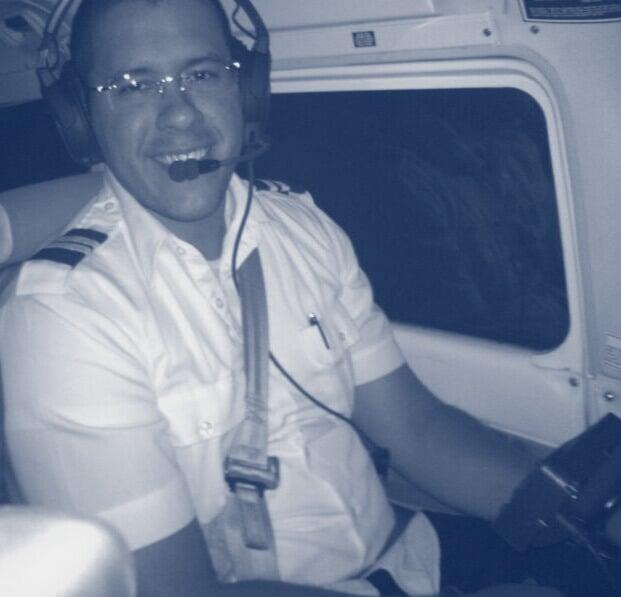

"I didn't become a pilot to sell insurance. I became licensed to serve the community I'm already part of, with the expertise and integrity you deserve." - Mauricio Machado | Founder

20 Years in Aviation

Florida Licensed Insurance Advisor

Long-Term Partnership Approach

Fiduciary Commitment

While insurance regulations only require "suitability," we operate at fiduciary standard, meaning your interests come first in every recommendation. We also work with only A+ rated and better carriers.

How We Work: Transparent, Educational, No-Pressure

Unlike traditional insurance sales processes, we start with education and understanding, not product pitching. Here's exactly what to expect when you work with us.

Three-Step Process

- Step 1: Free Educational Consultation: We start with a 30-45 minute conversation (phone or video) where I learn about your aviation career, your family situation, your financial goals, and your concerns. This is educational, not a sales pitch. You'll leave understanding your options whether you work with me or not.

- Step 2: Customized Recommendations: Based on our conversation, I'll research solutions that fit your specific situation, accounting for your aviation activity, income reality, and coverage needs. I'll show you multiple options with transparent pros/cons and full disclosure of how I'm compensated on each.

- Step 3: Implementation & Ongoing Support: If you choose to move forward, I handle the underwriting process (ensuring your aviation activity is properly disclosed), answer questions throughout, and remain available as your career and family evolve. This is a relationship, not a transaction.

Common Questions From Pilots About Life Insurance

Let's Talk About Protecting Your Family—Pilot to Pilot

You've built your life around aviation despite financial uncertainty, irregular income, and risks most people don't understand. You deserve insurance guidance from someone who's actually lived this reality, who speaks your language, understands your career, and serves your interests above sales quotas.

Your free consultation is educational, not transactional. You'll leave with clarity about your options whether you work with me or not. Because that's how pilots should be treated—with respect, transparency, and genuine expertise.